Demand Forecasting for Managers by Stephan Kolassa & Enno Siemsen

Author:Stephan Kolassa & Enno Siemsen [Kolassa, Stephan & Siemsen, Enno]

Language: eng

Format: epub

Publisher: Business Expert Press

Published: 2016-08-17T00:00:00+00:00

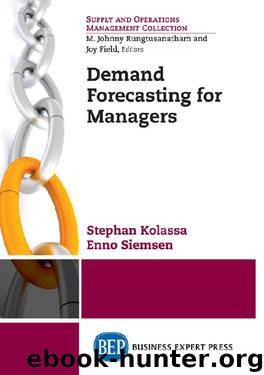

Figure 9.4 Single exponential smoothing applied to an intermittent time series

Remember that single exponential smoothing creates forecasts by calculating a weighted average between the most recent forecast and the most recent demand. Thus, the forecasts tend to drop and slowly move toward zero over time when no demand is observed. However, after demand is observed, forecasts briefly “jump” up again. Thus, our forecast is high right after a nonzero demand and low after a long string of zero demands.

This form of forecasting does not make sense in two important situations. First, consider a context where our intermittent demand is driven by a few customers that replenish this SKU when they need it; in this case, we would need a higher forecast (and not a lower forecast) after a long string of zero demands, because it becomes more likely that these customers will place an order again as more time passes. Second, if we have a context where the intermittent demand is driven by many customers buying independently, the forecast should not exhibit any time dynamics at all, because at any point in time, there is an equally large pool of customers that may soon demand the product. In addition, we will typically make replenishment or production decisions right after our stock has been depleted by a sale, so forecasts that are biased high right after sales will lead to particularly high reorder quantities and to unnecessarily high inventories. To overcome these problems, we will focus our attention now on a method that is designed to overcome these challenges.

9.3 Croston’s Method

Croston (1972) examines the problem of forecasting intermittent demand and proposed a specific solution to this problem. This solution is by now an industry standard and bears Croston’s name. Instead of exponentially smoothing the raw demands, we separately smooth two different time series: (1) all the nonzero demands from the original time series and (2) the number of periods with zero demands between each instance of nonzero demand. In a sense, we decompose the forecasting problem into the subproblems of predicting how frequently demand happens and predicting how high the demand is if it happens. We highlight the values associated with these two time series in Figure 9.5.

Download

This site does not store any files on its server. We only index and link to content provided by other sites. Please contact the content providers to delete copyright contents if any and email us, we'll remove relevant links or contents immediately.

Hit Refresh by Satya Nadella(9122)

The Compound Effect by Darren Hardy(8941)

Change Your Questions, Change Your Life by Marilee Adams(7753)

Nudge - Improving Decisions about Health, Wealth, and Happiness by Thaler Sunstein(7689)

The Black Swan by Nassim Nicholas Taleb(7104)

Deep Work by Cal Newport(7059)

Rich Dad Poor Dad by Robert T. Kiyosaki(6601)

Daring Greatly by Brene Brown(6501)

Principles: Life and Work by Ray Dalio(6413)

Playing to Win_ How Strategy Really Works by A.G. Lafley & Roger L. Martin(6219)

Man-made Catastrophes and Risk Information Concealment by Dmitry Chernov & Didier Sornette(6001)

Big Magic: Creative Living Beyond Fear by Elizabeth Gilbert(5753)

Digital Minimalism by Cal Newport;(5747)

The Myth of the Strong Leader by Archie Brown(5495)

The Slight Edge by Jeff Olson(5409)

Discipline Equals Freedom by Jocko Willink(5377)

The Motivation Myth by Jeff Haden(5202)

The Laws of Human Nature by Robert Greene(5170)

Stone's Rules by Roger Stone(5080)