How to Make a Fortune from the Biggest Bailout in U.S. History by Insana Ron

Author:Insana, Ron

Language: eng

Format: epub

Publisher: PENGUIN group

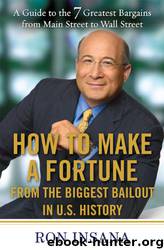

EQUITY RESIDENTIAL

(Source: BigCharts.com)

© Copyright 2009, Ned Davis Research, Inc.

Equity Residential’s market price has fallen on hard times, even though its underlying fundamentals remain solid. As you can clearly see here, the REIT is trading at levels last seen in the late 1990s, well before the property market went bust.

This is not a recommendation for Sam’s REIT. But the chart clearly illustrates that, like the underlying real estate market, REITs have been pounded.

Real estate values will not stay down forever, nor will the price of REITs. Buying a REIT with a generous, but not too generous, yield will not only offer potentially stable and attractive returns but also offer price appreciation, or a capital gain, if the world goes back to some version of normal. In the meantime, you are paid nearly 9 percent to wait.

I say that the yield, or more precisely the dividend yield, should not be too generous because, often, an extraordinary dividend yield could be a sign of trouble.

The dividend yield is, as explained earlier, the result of dividing the annual yield by the current market price of the REIT. When the dividend yield gets too high, it may indicate that the property manager is paying out an unsustainably large dividend. Think of it this way: the price of the REIT is falling because smart investors see trouble brewing in the REIT manager’s underlying business. Without adjusting the payout downward, the dividend yield begins to rise. (If the price of the REIT is falling but the dividend stays the same, the dividend yield will rise automatically.)

But that rising yield could be signaling that the payout will need to be cut because the fundamentals of the underlying properties are deteriorating. That happened to some key mall REITS in 2009, as shopping centers went begging for customers and lessors.

General Growth Properties, which went bankrupt in 2009, sported a dividend yield of over 37 percent at its peak, but that was not an attractive yield—it was, instead, a sign of impending doom.

Like any investment, real estate investment trusts come with some attendant risks, not the least of which is how a recession, or real estate bust, can affect the underlying business.

But given the decimation of REIT values, many REITs are being recommended by financial market analysts as attractively priced, with solid yields and improving fundamentals.

The same can be said of closed-end mutual funds that invest in real estate, such as Ken Heebner’s CGM Realty Fund.

Closed-end mutual funds trade on stock exchanges and also invest in real estate, seeking both attractive yields and capital appreciation.

Download

This site does not store any files on its server. We only index and link to content provided by other sites. Please contact the content providers to delete copyright contents if any and email us, we'll remove relevant links or contents immediately.

The Compound Effect by Darren Hardy(8978)

Tools of Titans by Timothy Ferriss(8403)

Nudge - Improving Decisions about Health, Wealth, and Happiness by Thaler Sunstein(7712)

Win Bigly by Scott Adams(7204)

Deep Work by Cal Newport(7092)

Rich Dad Poor Dad by Robert T. Kiyosaki(6646)

Principles: Life and Work by Ray Dalio(6466)

Pioneering Portfolio Management by David F. Swensen(6305)

Digital Minimalism by Cal Newport;(5769)

The Barefoot Investor by Scott Pape(5753)

Grit by Angela Duckworth(5623)

The Slight Edge by Jeff Olson(5421)

Discipline Equals Freedom by Jocko Willink(5394)

The Motivation Myth by Jeff Haden(5217)

You Are a Badass at Making Money by Jen Sincero(4935)

The Four Tendencies by Gretchen Rubin(4608)

Eat That Frog! by Brian Tracy(4546)

The Confidence Code by Katty Kay(4268)

Bullshit Jobs by David Graeber(4197)